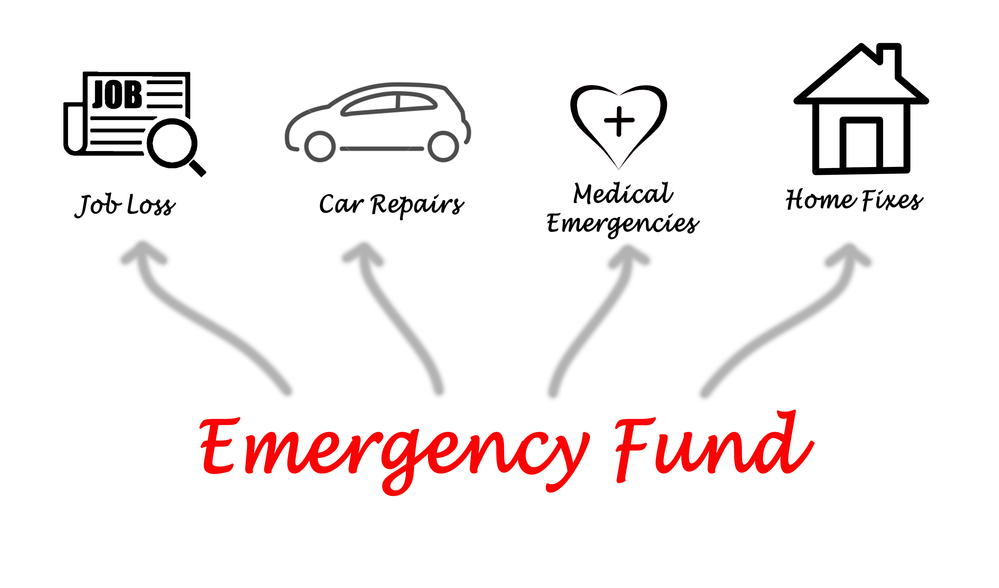

Now that many of you have taken part in our 52 Week Savings Challenge … you should, at this point, have at least a small START to an Emergency Fund. That Emergency Fund is going to be a resource for those unexpected costs that come up ~ for example.. a new water heater that broke out of the blue.

OR, in case a natural disaster hits your area. We don’t have those too much in Arizona, thankfully – but if you are a normal person with kids, a home and vehicles, chances are you have car issues, medical emergencies & more.. that might pop up out of nowhere.

But now that you HAVE this Emergency Fund, when do you USE it? Not ever situation is going to be a clear black and white emergency – so you will want to know what is so that you can preserve as much of that Emergency Fund as possible for what it’s truly meant for: An Emergency.

Here are some things to ask yourself to determine if you find yourself in this situation:

#1 ~ Is it Unexpected

Things often come up that you may feel the need to pull money from your emergency fund to pay for — an unexpected job loss tops the list. But regular events like Christmas shopping… or Back to School Preparation, or even a new baby — those occasions are not unexpected. In fact, in most cases you know about these events well in advance.

#2 ~ Is it Something you NEED

If you have a home problem with your air conditioner, and your air conditioner has suddenly stopped working or broke and it’s the heat of summer, then that IS worthy of pulling out of your emergency fund.

Don’t confuse a necessity with a want.. because they are so entirely different. It’s always nice to have new items, but it doesn’t mean that pulling from your emergency fund is required.

#3 ~ Is it Urgent

If it’s something that can wait, such as a new sofa, or television, you should probably save up for it instead of pulling from the emergency fund. If you are faced with painting the house because you hate the color then save – because that is far from being worthy of pulling out of your emergency fund.

Our Air Conditioner died two years ago – and in the middle of the summer, THAT was an Emergency – thankfully we had an Emergency Fund that helped us take care of that short term problem – and within a few weeks we had replaced that money with a few extra deposits.

So how much is enough to sock away?

The 52 week savings challenge is a great way to get your Emergency Fund started ~ 12 months allowed many of you to put away just over $1300.

But that’s not where it ends! Continue to keep saving so you can rack up at least 3 – 6 months of living expenses. .. you may also want to give some thought to how much that figure really is – by adding up your current income & expenses and determining how much you NEED to operate your household in one month.

Then multiply that by 3 – 6 for an extended period.

WHY do you Need One?

MANY people disregard them & claim they aren’t needed, but they ARE and should be a priority for your family.

I can’t tell you how many times we have relied on ours, and have been thankful we HAD one when we most needed it… with a family of 6, it’s one of the most important things for us to ensure is always there.

Having an emergency fund helps you stress LESS

When emergencies come up, often times than not, they are STRESSFUL. That is primarily due in part to living without that safety net! Most people stress because they know they don’t have the means necessary to bounce back – then, they resort to credit cards, which in turn creates it’s OWN stress – that’s a whole different beast!

Be prepared – plan NOW, commit to SOMETHING, and be consistent – you’ll find yourself worry MUCH less when an emergency arises.

Having an emergency fund prevents you from unnecessary spending

Keep that money out of reach – a separate bank account, and something that might be a little harder to get to, especially if you can’t help but want to touch it. Wanting to buy new things is NOT an emergency – hold onto that money and keep it available for those times that DO require you to break out the extra cash: Job Loss, Car problem or, perhaps a Medical Emergency.

Having an emergency fund helps prevent you from making incredibly poor financial decisions

Having the ability to use a plastic credit card is NOT a good financial decision – in fact, leaning on credit is NEVER a good choice, no matter who you are. Why rely on that when you can rely on yourself with a little foresight & planning?

Sure, you might think that you can pay it off monthly, but it’s not without fees, interest and possible penalties. If you are that disciplined that you can justify a credit card, then you surely SHOULD have the long term discipline to commit to a monthly savings in your Emergency Fund.

Leave a Reply

You must be logged in to post a comment.